In moments of geopolitical conflict, financial markets tend to react intensely. Sharp swings in stock markets, surges in commodity prices, and unexpected changes in interest rates often dominate headlines. For investors, this environment can seem like a call to immediate action — selling assets, seeking safe havens, or trying to anticipate opportunities.

However, the history of markets suggests something counterintuitive. During periods of war and international crisis, the most efficient strategy for most people may simply be to remain calm and avoid impulsive moves. This approach, based on decades of academic evidence and the historical behavior of markets, challenges the idea that it is necessary to react quickly to protect or maximize investments.

At the same time, the current scenario presents new elements that require careful analysis. The growing concentration of the American stock market, the dominant role of the technology sector, and the strategic relevance of oil in international conflicts add layers of complexity that cannot be ignored.

The temptation to act amid chaos

When armed conflicts arise, especially those involving global powers or regions that are strategic for energy supply, investors often shift into defensive mode. The natural impulse is to try to predict the economic impact of the war and reposition portfolios quickly.

The logic seems simple. If the price of oil rises, buying shares of energy companies could generate gains. If uncertainty increases, investing in gold or government bonds may offer protection. And in moments of extreme volatility, exiting the market entirely may appear to be the most prudent decision.

The problem is that this approach requires something extremely difficult: getting the timing right. To obtain consistent returns with opportunistic strategies, it is necessary to know exactly when to enter and when to exit the market. Even professional investors frequently fail at this task.

Academic studies show that most long-term returns in financial markets are concentrated in a small number of specific days of strong appreciation. Investors who try to avoid downturns often end up missing these recovery moments.

The power of inertia in the long term

Over the last century, the American stock market has shown a predominant upward trend despite wars, financial crises, natural disasters, and political shocks. This trajectory has not been linear; there have been periods of sharp decline and deep recessions, but the general direction has remained positive.

Historically, maintaining diversified and low-cost investments has been an effective strategy for capturing global economic growth. Broadly diversified index funds, for example, allow investors to follow market performance without the need to predict specific events.

Jeffrey Yale Rubin, president of Birinyi Associates, an independent stock market research and investment firm in Westport, Connecticut, highlighted this truth in a brief report to clients.

Mr. Rubin examined the reaction of stock and oil markets to all “past American attacks lasting more than one day,” beginning with “Operation Desert Storm,” the U.S.-led war to expel Saddam Hussein’s Iraqi forces from Kuwait. That war began in mid-January 1991. It was short and, according to most accounts at the time, a resounding success.

There have been seven more American military campaigns lasting more than one day since then, up to the current war with Iran. They have varied geographically, in intensity and duration, including conflicts in Bosnia, Iraq, Kosovo, Afghanistan, Libya, and Syria.

What Mr. Rubin found was surprising. One year after the start of those conflicts, the S&P 500 index, on average, had risen 12.5%. This compares with an average annualized return (excluding dividends) of the S&P 500 of only 9%. In an email, Mr. Rubin stated: “In summary, geopolitical events similar to the current period have historically produced above-average returns one year later.”

In other words, this does not mean that wars are irrelevant to the economy. On the contrary. But it indicates that the market often anticipates negative scenarios and then adjusts expectations as new information emerges. Although the stock market has often, but not always, declined in the weeks following the start of a conflict in the United States or other geopolitical shocks, stocks generally recover and begin rising again quickly. Keeping costs low and investing in the stock market has proven advantageous over the long term.

The crucial role of oil

If the stock market tends to show resilience over time, the same cannot be said of the energy market. Conflicts in the Middle East, for example, have historically caused strong fluctuations in oil prices.

This happens because the region concentrates strategic routes for the transportation and production of fossil fuels. The Strait of Hormuz, for example, is responsible for the transit of about one fifth of the oil and natural gas traded globally.

When tensions threaten this infrastructure, energy prices can surge. This increase tends to generate higher inflation, pressure central banks to raise interest rates, and reduce the purchasing power of households.

Oil prices surged in the current conflict, as in many previous conflicts. In addition, one year after the start of military action, Mr. Rubin found that the price of Brent oil, the benchmark for oil outside the United States, had also risen. The average price increase was substantial, at 27%. This often triggers higher inflation. And surging oil prices have led to recessions, especially in earlier periods, such as the 1970s and early 1980s.

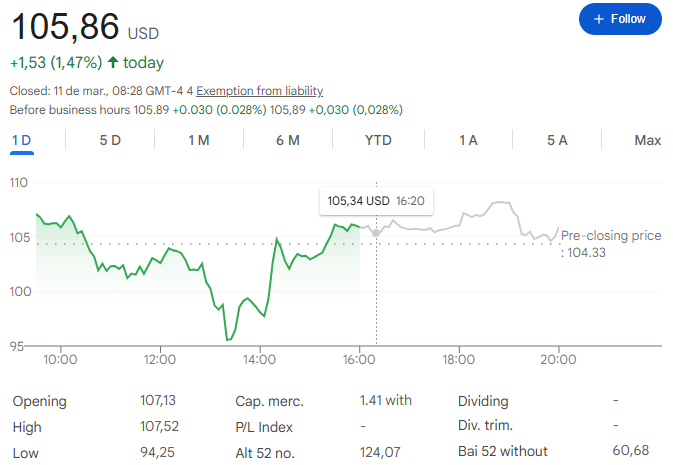

Perhaps anticipating current problems in the Middle East, the S&P 500 energy sector experienced a strong rise in the weeks leading up to the war. The increase was more than 26% from the beginning of the year through March 2, compared with a small decline in the S&P 500 index as a whole. Exxon Mobil, the oil giant, rose more than 25% through Tuesday. The United States Oil Fund ETF, which holds oil futures contracts, posted a similar increase.

Although the global economy — and the U.S. economy in particular — is not as dependent on oil as it was 50 years ago, a large and prolonged oil shock could be damaging. Because the United States is now a net exporter of oil and natural gas, the American energy sector could obtain extraordinary profits. But rising prices would hurt American consumers and the rest of the economy.

For investors, this creates a paradox. While companies in the energy sector may benefit directly from conflicts, the negative impact on consumers and other sectors of the economy can limit broader gains in the stock market.

A more concentrated and more expensive market

Another factor that differentiates the current scenario from previous crises is the structure of the financial market. In recent years, enthusiasm for emerging technologies such as artificial intelligence has strongly boosted the value of major technology companies.

This movement has resulted in a significant concentration of the American stock market in a small group of companies. When a few assets represent a large share of the total market value, the system becomes potentially more vulnerable to changes in expectations.

High valuations can also amplify negative reactions. If investors begin to question the future growth of these companies, declines may be more intense than in periods of more moderate valuations.

This context does not invalidate the long-term strategy based on inertia. But it suggests that structural risks may be greater than in previous cycles.

The impact on bonds and interest rates

International conflicts also directly affect the fixed-income market. The possibility of higher inflation, driven by rising energy prices, may lead central banks to maintain or raise interest rates.

This influences the yield of U.S. Treasury bonds, considered a global benchmark of financial safety. During periods of war, investors often seek these assets for protection, which can temporarily reduce yields.

However, if inflation expectations increase, interest rates may rise again. This movement has important implications for mortgage financing, consumer credit, and corporate investment.

In addition, the strengthening of the dollar often accompanies scenarios of international tension, especially when the United States is perceived as a safe haven for global capital.

The importance of diversification and liquidity

Faced with so many variables, the most consistent recommendation for long-term investors continues to be maintaining diversified portfolios. This includes exposure to global stocks, high-quality bonds, and sufficient liquidity reserves to face periods of instability.

Having money in safe assets — such as government-insured bank accounts or government bonds — allows investors to go through crises without needing to sell assets at unfavorable moments.

This preparation is essential because, although markets historically recover, the time required for that recovery can vary. Investors who need to access resources during downturns may suffer permanent losses.

When to adjust the strategy

Despite the strength of the argument in favor of inertia, there are situations in which adjustments may be necessary. Structural changes in the global economy, technological transformations, or significant shifts in monetary policy may justify strategic revisions.

Prolonged conflicts that affect supply chains, energy infrastructure, or international financial stability may also require more active responses.

The key lies in distinguishing between short-term noise and fundamental changes. Daily fluctuations in markets rarely indicate permanent transformations. Persistent trends in inflation, economic growth, or public policy, however, may require adaptation.

Hope for the best, prepare for the worst

Investing during periods of war involves dealing with deep uncertainty. No economic model can accurately predict the duration of conflicts or their political consequences.

Even so, historical experience suggests that economies and markets possess a remarkable capacity for recovery. Companies continue innovating, consumers continue spending, and governments adjust policies to stimulate growth.

For investors, the central lesson remains surprisingly simple. Maintaining discipline, diversification, and long-term focus is usually more effective than reacting impulsively to every piece of news.

This does not mean ignoring risks. It means recognizing that, in many cases, the best strategic decision is to resist the temptation to act.

In an increasingly volatile world, this may be the most rational attitude — and, paradoxically, the most difficult one to adopt.