In times of economic crisis and geopolitical tension, investors tend to seek clear signals from monetary authorities. They expect decisive actions, strategic interest rate cuts, or emergency measures capable of stabilizing volatile markets. However, at specific moments in economic history, the best decision a central bank can make may be precisely not to act.

This is the current situation faced by the Federal Reserve, the central bank of the United States. Amid rising energy prices driven by conflicts in the Middle East, persistent inflation above target, and uncertainty generated by aggressive trade policies, maintaining interest rates — without immediate cuts — may represent the only prudent strategy.

Although at first glance this may seem contradictory, a rate cut at this moment could be interpreted as an alarming signal: recognition that the economy is entering a deep crisis. For investors, consumers, and businesses, the absence of changes in monetary policy may be less a sign of inertia and more an attempt to preserve stability in a risk-filled environment.

The delicate role of the Federal Reserve in times of turbulence

The role of the Federal Reserve is simultaneously simple and complex: to control inflation and promote full employment. Under normal conditions, these goals can be balanced through gradual adjustments in interest rates. When the economy slows, lowering rates stimulates consumption and investment. When inflation accelerates, raising rates helps contain demand.

In the current context, however, the situation is more ambiguous. Recent indicators point to fragile economic growth, with a slowdown in job creation and modest stock market performance. Under traditional circumstances, these signals could justify a more expansionary monetary policy.

At the same time, the sharp increase in energy prices — a direct result of military tensions and disruptions in global supply — pushes inflation upward. Cutting rates in an inflationary environment could worsen the problem, fueling expectations of persistently rising prices.

This combination of risks places the central bank in a delicate position. The monetary authority needs to wait for new data to assess the magnitude of the economic shock before making decisions that could have lasting consequences.

The impact of oil and commodities on the global economy

Since the beginning of the conflict in the Persian Gulf, the prices of oil, gasoline, and liquefied natural gas have recorded sharp increases. Other strategic commodities, such as fertilizers and food, have also shown an upward trend, reflecting the interdependence of global supply chains.

Although the United States is currently one of the world’s largest energy producers, the country is not immune to the effects of these shocks. Rising fuel costs increase transportation and production expenses, reduce household purchasing power, and put pressure on businesses across various sectors.

In regions more dependent on energy imports, such as Europe and parts of Asia, the effects can be even more intense. The shortage of natural gas and rising oil prices create an environment conducive to economic slowdown and financial instability.

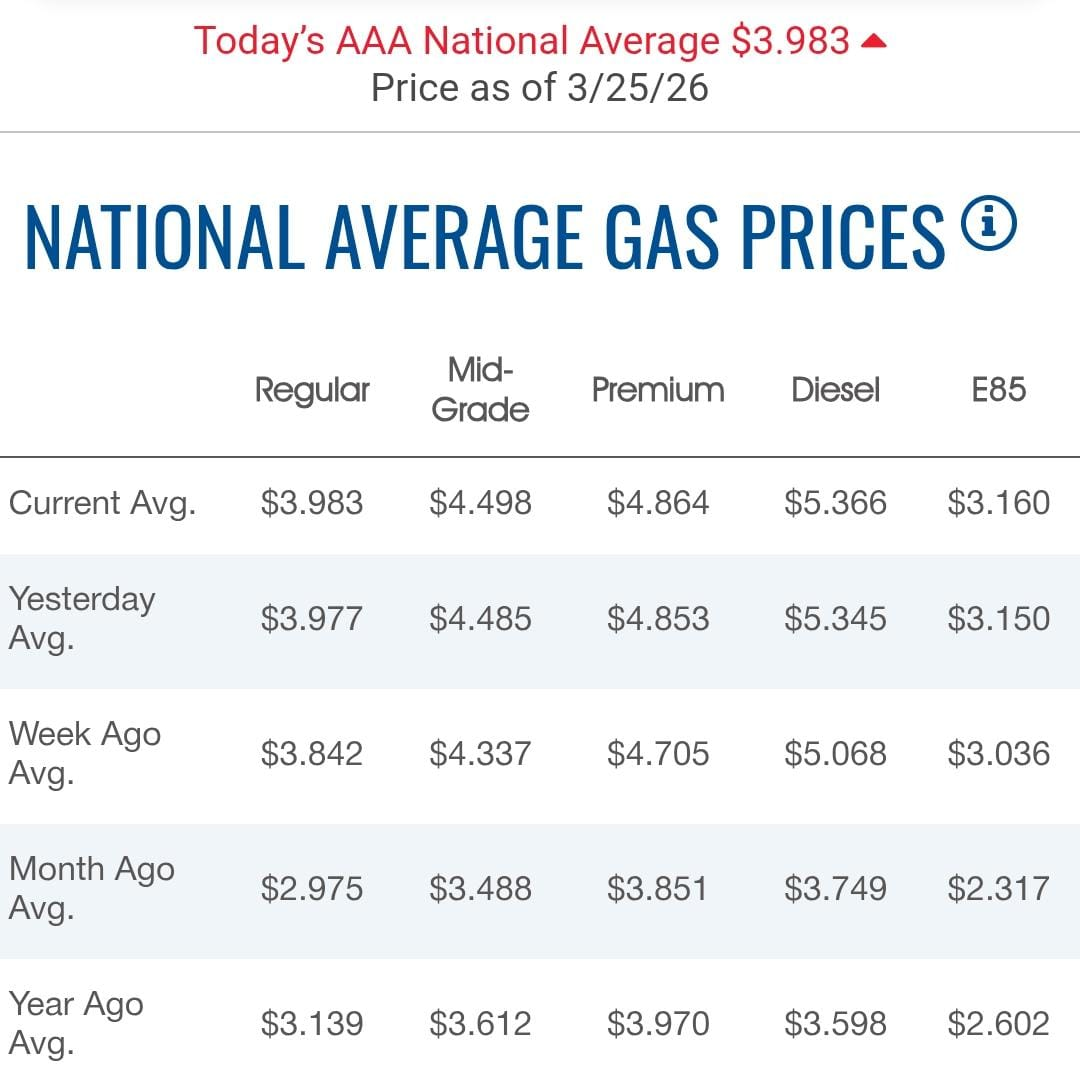

Historically, prolonged energy shocks have been associated with periods of high inflation and recessions. During the crisis triggered by the invasion of Ukraine in 2022, for example, the price of Brent oil exceeded $120 per barrel, but only in June. The price of unleaded gasoline at gas stations surpassed $5 that month, according to AAA, and the inflation rate in the United States, measured by the Consumer Price Index, rose above 9%. This was the highest inflation rate in the country since the oil shocks of the 1970s and 1980s.

Although the contemporary economy is less dependent on oil than it was in the 1970s and 1980s, the strategic importance of routes such as the Strait of Hormuz — through which about one fifth of the world’s oil passes — keeps the market sensitive to supply disruptions.

Inflation and the risk of unanchored expectations

One of the greatest concerns of monetary policymakers is the so-called unanchoring of inflation expectations. This phenomenon occurs when consumers and businesses begin to believe that prices will continue to rise rapidly in the future.

When this perception becomes established, economic behavior changes. Workers demand higher wages, companies raise prices preemptively, and investors demand higher returns to compensate for the loss of purchasing power. The result is an inflationary cycle that is difficult to stop.

Since the period when Paul Volcker led the Federal Reserve at the end of the last century, avoiding this scenario has become a central priority for central banks around the world. At that time, drastic measures were necessary to contain inflation, including extremely high interest rates that triggered deep recessions.

Today, although inflation is below the most critical historical levels, the risk of acceleration remains. If energy prices continue to rise and trade policies increase import costs, the Federal Reserve may be forced to maintain a restrictive stance for longer than the market expects.

The other specter: the possibility of recession

Inflation is not the only challenge. The persistent increase in energy costs also raises the risk of recession. When fuels and essential inputs become more expensive, companies reduce investment, consumers cut spending, and economic growth weakens.

Recent economic models suggest that the probability of a significant slowdown had already been increasing even before the escalation of geopolitical tensions. The oil shock only intensifies this trend.

Predicting recessions is notoriously difficult, and the signals are often ambiguous. In recent years, conflicting indicators have alternated between optimism and pessimism, without a deep economic contraction materializing.

Still, the risk cannot be ignored. If the economy faces a financial collapse or a sharp decline in activity, the central bank may be forced to act quickly, lowering rates and adopting emergency measures to prevent greater damage.

Monetary policy, fiscal policy, and regulatory uncertainty

In addition to international tensions, the American economy faces uncertainties related to trade and fiscal policies. Tariffs on imports, legal disputes, and diplomatic negotiations create an unpredictable environment for businesses and investors.

This is not something the Fed can completely ignore, but the central bank, still led by Jerome H. Powell, is struggling to maintain its independence in the face of President Trump’s demands for drastic interest rate cuts. Powell’s term as Fed chair ends on May 15. However, Kevin Warsh, nominated by President Trump as Powell’s successor, may not be confirmed by the Senate by that date. Powell said on Wednesday that he expects to continue as Fed chair temporarily if that happens.

Therefore, the Fed is in a difficult position. It is hard to imagine how an independent central bank, facing an inflationary threat, could reduce interest rates now. But a recession, or a financial collapse, would immediately change that scenario.

Historically, the credibility of monetary authorities plays a fundamental role in financial stability. Any perception of political interference can affect market expectations and increase volatility.

What investors should expect now

For long-term investors, the current scenario requires caution and patience. The temptation to react quickly to every geopolitical development or monetary decision can result in impulsive strategies and financial losses.

The Federal Reserve’s decision to maintain interest rates can be interpreted as a sign of prudence. Rather than seeking immediate stimulus, the central bank appears to prioritize gathering information and carefully assessing risks.

In many cases, periods of apparent monetary calm — without sharp cuts or increases — allow markets to gradually adjust to new economic conditions.

This does not mean the absence of risks. Fluctuations in asset prices, changes in inflation expectations, and unexpected events can quickly alter the outlook. However, hasty decisions based on fear or euphoria tend to be more harmful than helpful.

A moment of global economic transition

The world is going through a phase of profound transformation, marked by regional conflicts, technological changes, and the reconfiguration of supply chains. In this context, traditional monetary policies may face unprecedented limitations.

For the Federal Reserve, the most sensible strategy may be to avoid dramatic actions until the extent of economic shocks becomes clearer. For investors, understanding this logic is essential to navigating an environment of growing uncertainty.

Ultimately, financial stability depends not only on government decisions, but also on collective confidence in the ability of institutions to face complex crises.

If the Central Bank’s silence is capable of preserving that confidence, it may paradoxically become the best news the markets could receive.